July 2022

Since I started WealthLander at a time of irrational exuberance and extreme bullishness in January 2021, this is the best period I’ve seen to make a case for a new bull market in equities. This may relieve some of my followers who were used to seeing my bearish outlook in one article after another! This article will highlight the real bull case. Nonetheless, I still discard the usual bull market argument you’ve heard repeated a thousand times before in the hope that repetition will make you believe it and highlight the importance of being more selective.

But don’t despair – the bear is still here today – so I will also argue what the continuing big bear market case is for markets. Of course, I will be grossly redacting the current state of the world – which is incredibly nuanced and complicated – in favour of highlighting what is generally underappreciated, crucially important, and not given enough emphasis elsewhere in decision-making. You can make up your mind about what works for you, but I will highlight why I think it is essential to have a balanced and broader perspective, and not be all in or all out of cash.

The Bull Case for Markets

The Common Bull Market Reason to Invest Today

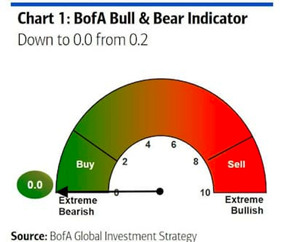

“Buy when there is blood in the streets”. Investors are bearish, and no one wants to invest. Many active managers are down 50% or more from their highs in 2021 and have suffered heavy redemptions. Numerous market indicators indicate extreme bearishness. If it feels uncomfortable to invest right now, that’s precisely why this is the time to invest – before it gets more comfortable.

The potential problem with this view – which would otherwise be sensibly contrarian – is although investors feel bearish, they are still positioned quite bullishly. Usually, at the end of bear markets, investor allocation to equities is 20% below where it is today and equities are loathed. That is not the case today – Investors feel crappy about the outlook but haven’t yet withdrawn in mass from markets (and may not). There hasn’t been any capitulation, but merely a grinding and slow bear market as liquidity is removed.

Nonetheless, this bull case is a whole lot better than the usual bull market case where markets always go up! Don’t be fooled by this market propaganda– look back a century, and you will find many long-term periods when markets didn’t go up and where many markets were effectively nationalised or destroyed (for example, by being vanquished in war). Hence saying markets always go up is a simple case of selection bias and misleading marketing.

The Real Case for a Bull Market

The real reason to be bullish is based on two factors which are not yet widely appreciated:

(1) The first – and most important – is that central banks may soon be forced to give up on tightening financial conditions aggressively, and that markets will begin to anticipate this as underlying inflationary pressures are already easing and the economic outlook is rapidly deteriorating. Central banks will slow down the rate hiking cycle or stop it and hence fail to meet or exceed aggressive investor expectations for interest rate hikes, i.e. central banks will be more dovish than bond markets have been pricing in.

Interest rate hikes have to stop at some stage because vast amounts of unproductive debt mean that unless central banks want widespread defaults and a deflationary economic collapse (they almost certainly don’t), they have to eventually err on the side of tolerating some inflation to whittle away the debt through nominal inflation and currency (cash) and bond (fiat) depreciation (in real terms). We live in a credit-drive and Ponzi-like global economy which demands easy money to continue to avoid a “Minsky Moment”, with the alternative being the Minsky moment – doing the same until the Minsky Moment is unavoidable. The Minsky Moment may be inevitable, but it is likely not (at least in our view or that of most informed parties) unavoidable today. Human action (central bank tightening) is the main factor driving today’s difficult markets, and this human action can be ceased on a whim.

Of course, any caring human would prefer policy be built around more equitable economies focussed on real productivity and real economic growth rather than fake wealth and easy money, but alas that hasn’t been the emphasis of policy in recent decades. This is unlikely to change soon given the state of the world and bureaucratic and political emphasis in many countries. As investors, we need to cope with the hands we’ve been dealt even if politically and socially we are outraged with the historic misdirection and misallocation of capital, and hence a waste of opportunity to build more productively for our future. We obviously need to be more productive as populations age and in the face of geopolitical threats to the status quo (which have been so beneficial to Western economies in times past and allowed us to become so complacent).

(2) The second reason to be less bearish or long-term bullish is that many assets are worth buying on valuation grounds alone today. It is easy to find suitable long-term value in markets today, even when many other assets remain overpriced. Examples of good value assets with fundamentally strong outlooks over the medium term include many inflationary assets (highlighted in my previous Livewire articles), which have done relatively well in recent months but have been recently sold off in response to a recession being priced in and China woes. Research-based active, fundamentally researched, and value-orientated managers hence have a better long-term outlook. Valuation doesn’t help much with short-term returns. Still, it does suggest longer-term returns are likely to be satisfactory for those who value what they buy and who purchase good quality assets.

The fate of more passive or index-like investors who don’t value anything and may buy everything is more dependent on markets as a whole. Many equity markets still impute low long-term returns, and hence their investors can continue to expect mediocre long-term returns, even if short-term returns improve.

The Case for Persistent Bearishness and a Prolonged Bear Market

There are two big unappreciated reasons for being persistently bearish (again, the first relating to the next few weeks and months, and the second having a multi-year relevance):

(1) We are heading for imminent recession, and Central Banks are making a huge policy mistake – continuing to tighten into a recessionary and stagflationary environment (potentially for political reasons but also because currently, inflation appears out of control). The last two quarters in the US may illustrate a technical recession, and leading indicators are rolling over fast, suggesting central banks may well get the reduced demand needed to slow current inflationary pressures they’ve been looking to create, and soon – but will it be enough for them to stop their current trajectory? Long-term inflationary expectations are not high. Yet Central Banks are committed to imminent hikes and will hike – as they have in every other cycle – until something big breaks. Furthermore, we should rely on current central banks being backwards-looking, unreliable and making huge policy mistakes – as they have persistently demonstrated in recent years!

The fringes are already broken, including entire countries, and preeminent economies are under immense stress, e.g. emerging markets such as Sri Lanka, cryptocurrency exchanges, Chinese mortgagees, and European energy policy. The Russia-Ukraine conflict and geopolitical tensions are unresolved and could unexpectedly escalate. Investors are still heavily allocated to risk assets, even if they feel bearish, and may hence be about to capitulate – deciding to redeem in mass when there are one too many interest rates increases and if central banks demonstrate they are more committed to killing inflation than bailing out asset prices….

(2) Bear Markets which coincide with recession are usually longer and larger than a simple 20% drawdown, averaging about 33% losses. Given where valuations have come from and the economic fragilities, we should expect losses to be at least the average of circa one-third from the peak in such circumstances with any normalisation of monetary policy. Many investors have been conditioned to using the last 20 years of data rather than considering the stagflation of the 1970s, the post-war supply-side constrained 1940s, or the early 1990s Australian recession when considering the derating potential of market valuations in an inflationary environment. Indeed, losses could eventually exceed 50% in worst-case scenarios. We should hence expect more pain from current conditions.

In summary, the bull case relies on central banks realising they need some inflation to prolong the Ponzi, and destroying further demand is a hazardous policy in current circumstances and not useful to the main need to continue an era of financial repression – keeping interest rates low but debt holders whole. The bear case relies upon continuing to bet on more central bank hikes despite the mounting evidence they’ll kill the economy. Both have a case; hence, the outlook is nuanced and unsuitable for any extreme positioning. Some investors have gone entirely to cash (effectively betting on a prolonged bear market or a depression), however currently, we prefer to take a medium-term outlook with a more inflationary bias, backing the case that central banks are about to slow or cease their current trajectory, or if central banks are a little slow to get it, they’ll fairly quickly be forced to attempt to right the ship as a crisis will make them. We hence see supply starved commodities as good value already with a strong fundamental medium-term outlook. We are warming to equity positions; particularly should we see signs of real market capitulation and/or policy change. We reiterate – some policy change (versus expectations) is more likely than not coming soon (within weeks or months), and investors are likely better off investing something now or gradually easing in than not being invested at all or being late once a policy change is effected.

Remember, small losses are much better than big ones and are quickly recoverable. It remains a risky world with a wide range of outcomes, so if you are investing, it is prudent to invest with those who emphasise risk management and who haven’t demonstrated a predisposition to setting large amounts of your money on fire.

Investors who’ve gone to cash will do what investors who’ve gone to cash always do – and not get back into markets early enough when the opportunity is there. An opportunity is quite possibly already here now or shortly – this month or next. Being excessively invested in cash is also unnecessary when there are alternatives to being invested which have already demonstrated their ability to reduce the equity downside and provide some positive return expectation over a reasonable time frame, even in the challenging market conditions of the recent past. Extrapolating the past is what central banks do, and I’m sorry, but those lucrative positions are already taken – Don’t be a central banker with your money, but equally, don’t go all in fighting the FED!

DISCLAIMER: WealthLander Pty Ltd ACN 646 957 119 is a corporate authorised representative (CAR; WealthLander) of Boutique Capital Pty Ltd (BCPL) ACN 621 697 621 AFSL 508011, CAR Number 1285158. CAR is the investment manager of the WealthLander Diversified Alternative Fund (Fund).

To the extent to which this document contains advice it is general advice only and has been prepared by the CAR for individuals identified as wholesale investors for the purposes of providing a financial product or financial service under Section 761G or Section 761GA of the Corporations Act 2001 (Cth).

The information herein is presented in summary form and is therefore subject to qualification and further explanation. The information in this document is not intended to be relied upon as advice to investors or potential investors. It has been prepared without considering personal investment objectives, financial circumstances or particular needs. Recipients of this document are advised to consult their own professional advisers about legal, tax, financial or other matters relevant to the suitability of this information.

The investment summarised in this document is subject to known and unknown risks, some of which are beyond the control of CAR and its directors, employees, advisers or agents. CAR does not guarantee any particular rate of return or the performance of the Fund, nor do CAR and its directors personally guarantee the repayment of capital or any particular tax treatment. Past performance is not indicative of future performance.

The materials herein represent a general summary of CAR’s current portfolio construction approach. Depending on market conditions and trends, CAR may pursue other objectives or strategies considered appropriate and in the best interest of portfolio performance.

There are risks involved in investing in the CAR’s strategy. All investments carry some level of risk, and there is typically a direct relationship between risk and return. We describe what steps we take to mitigate risk (where possible) in the Fund’s Information Memorandum, which must be read prior to investing. It is important to note that despite taking such steps, the CAR cannot mitigate risk completely.

This document was prepared as a private communication to clients and is not intended for public circulation or publication or for the use of any third party without the approval of CAR. While this report is based on information from sources that CAR considers reliable, its accuracy and completeness cannot be guaranteed. Data is not necessarily audited or independently verified. Any opinions reflect CAR’s judgment at this date and are subject to change. CAR has no obligation to provide revised assessments in the event of changed circumstances. To the extent permitted by law, BCPL, CAR and its directors and employees do not accept any liability for the results of any actions taken or not taken on the basis of information in this report or for any negligent misstatements, errors or omissions.

This Document is for informational purposes only and is not a solicitation for units in the Fund. Application for units in the Fund can only be made via the Fund’s Information Memorandum and Application Form.